Q1 2026 Market Review

- Girish Appadu

- May 12

- 9 min read

Global financial markets experienced a volatile first quarter, marked by a clear shift in macro regime. The dominant driver of performance moved away from growth and liquidity support toward inflation dynamics and geopolitical risk. This transition resulted in higher cross-asset volatility and less reliable diversification across traditional asset classes.

Macroeconomic Environment & Regime Shift

Markets entered the quarter supported by continued strength in AI-related equities and early signs of broader participation beyond mega-cap technology. However, sentiment deteriorated following two key developments: escalating geopolitical tensions in the Middle East and renewed shifts in global trade policy.

The geopolitical escalation had a direct impact on global energy markets, with Brent crude rising sharply as supply chains came under pressure. The oil price shock became the primary transmission mechanism into broader financial markets, driving a rapid repricing of inflation expectations and shifting the outlook for monetary policy from anticipated easing toward potential renewed tightening in select developed markets.

This marked a clear transition toward a more inflation-sensitive and macro-driven investment environment.

Commodities

Commodities were the strongest-performing asset class over the quarter, with the Bloomberg Commodity Index rising by more than 24%, led predominantly by energy markets.

Crude oil and natural gas accounted for the bulk of the gains, reflecting tighter supply conditions and heightened geopolitical risk premia. Some secondary price pressures were also observed in agricultural commodities, influenced by disruptions in global shipping routes and supply chain sensitivities.

Overall, the commodity rally reinforced global inflation concerns and contributed to a broad reassessment of central bank policy expectations.

Fixed Income

Global bond markets came under pressure as inflation expectations rose and interest rate expectations were revised higher.

Developed market sovereign yields increased across the curve, with the most pronounced moves at the shorter end, reflecting shifting expectations around policy rates. Markets moved away from pricing near-term easing and instead began to consider the risk of policy tightening persisting in certain regions.

Regionally, energy-importing economies such as Europe and Japan experienced greater upward pressure on yields due to imported inflation effects. In contrast, the US market was relatively more resilient, supported by softer labour market momentum and its position as a net energy exporter.

Credit markets also weakened in line with higher risk-free rates:

Investment grade spreads widened moderately

High yield bonds underperformed due to greater sensitivity to macro conditions

Emerging market debt was pressured by US dollar strength and tighter global liquidity conditions

Equities

Equity markets transitioned from earnings- and AI-driven momentum to a more challenging macro-driven environment.

US equities, particularly mega-cap technology names, declined as investors reassessed valuations in the context of higher rates, AI-related capital expenditure intensity, and margin sustainability.

European equities underperformed, reflecting higher energy costs, margin pressure, and weaker growth momentum.

Japan relatively outperformed, supported by a weaker yen, ongoing corporate governance improvements, and expectations of supportive fiscal policy.

Emerging markets were broadly flat to slightly negative, as early gains linked to technology exposure were offset by geopolitical uncertainty and inflation pressures stemming from higher commodity prices.

Factor performance reflected a more defensive posture among investors:

Value outperformed growth

More defensive, cash-generative companies outperformed long-duration equities

Volatility increased across equity styles

FX & Cross-Asset Behaviour

The US dollar strengthened over the quarter, reflecting safe-haven demand as well as relative interest rate and growth differentials versus other developed markets.

Traditional defensive asset behaviour was less consistent than in previous risk-off episodes:

Gold traded in a relatively narrow range and did not provide strong crisis hedging, as real yields rose and positioning became more tactical

The Japanese yen weakened despite risk-off conditions, reflecting policy divergence and structural capital flows

Cross-asset correlations increased, with equities and bonds declining simultaneously during periods of stress

Summary

Q1 2026 was defined by a clear shift in market regime, from liquidity- and growth-supported conditions to an environment dominated by macroeconomic and geopolitical forces.

Key themes included:

Energy-driven inflation pressures

A reassessment of central bank policy trajectories

Reduced effectiveness of traditional equity-bond diversification

Elevated cross-asset volatility and factor dispersion

In this environment, portfolio outcomes were increasingly driven by asset allocation decisions rather than directionality within individual asset classes. This reinforces the importance of active risk management, diversification across drivers of return, and flexibility in portfolio positioning.

Macroeconomic Outlook

GDP growth

Global GDP growth is expected to slow in 2026 relative to 2025 across most major regions, with the exception of the United States. US resilience is supported by fiscal policy support and the lagged impact of monetary policy easing delivered in 2025.

The downward revision to global growth reflects a combination of persistent supportive factors partially offsetting negative geopolitical shocks. These include reduced tariff pressures, existing policy accommodation, and positive carryover effects from stronger-than-expected economic performance in late 2025.

For 2027, global growth is expected to recover to approximately 3.2%, supported by easing inflation, a gradual normalisation following geopolitical disruptions, and more accommodative financial conditions as war-related economic drag diminishes.

Real GDP growth forecasts (% change, yoy)

Annual real GDP growth rates from 1980 to 2030 for the major economies

Inflation expectations

Global inflation is projected to pause its disinflationary trend, with headline inflation expected to increase temporarily in 2026 before moderating again in 2027. The near-term pickup reflects renewed pressure from higher energy and food prices, alongside persistent services inflation across major economies.

Inflation dynamics remain uneven across regions.

In the United States, inflation is expected to rise in the near term, supported by resilient domestic demand and wage pressures. Over time, inflation is projected to gradually converge toward target as labour market conditions normalise and productivity gains contribute to disinflationary pressures.

In the Eurozone, inflation is expected to remain above target through 2027. However, weaker growth momentum and easing energy price pressures should support a gradual moderation over the forecast horizon.

In the United Kingdom, inflation is expected to temporarily rise toward approximately 3.6%, before easing by end-2027. Near-term persistence is driven by elevated services inflation and tight labour market conditions.

In Japan, inflation is expected to moderate as imported food and commodity price pressures ease, following earlier cost-push dynamics. In contrast, China is expected to experience a gradual increase in inflation from currently subdued levels, reflecting a normalisation from historically low inflation conditions.

Inflation Expectations (%)

Core inflation trends across major economies (US, EA, UK, China, and Japan) from 2021 to 2026

From a structural perspective, inflation dynamics over the past decade reflect a significant regime shift. The post-2021 period was characterised by a global inflation surge, with developed markets experiencing synchronised spikes in 2022, most notably in the UK, Eurozone, and US, before a broad disinflationary phase emerged through 2023–2025. This adjustment has been uneven across regions, with the UK sustaining relatively higher inflation, while China and Japan have remained comparatively low and stable throughout the cycle.

More recently, core inflation across major economies has normalised toward more moderate levels, although persistence in services inflation continues to limit convergence to central bank targets in several developed markets.

Looking ahead, global inflation is expected to increase modestly from approximately 4.1% in 2025 to 4.4% in 2026, before easing in 2027. The near-term rise is driven primarily by higher energy and food prices, reflecting supply-side disruptions linked to recent geopolitical developments affecting key energy infrastructure and trade routes, including heightened volatility in global oil flows and maritime chokepoints.

Interest rates expectations

Interest rate expectations for 2026 reflect increasingly divergent inflation and growth trajectories across major economies, resulting in a more asynchronous global monetary policy cycle.

In the United States, policy rates are expected to remain elevated through the first half of 2026 before gradually easing in the second half of the year. This reflects the Federal Reserve’s cautious stance in the face of resilient domestic demand, persistent wage pressures, and sticky services inflation.

The United Kingdom is also expected to maintain relatively elevated policy rates through 2026, supported by ongoing labour market tightness and persistent services inflation, which continue to limit the pace of monetary easing.

In the Eurozone, policy rates are projected to remain relatively firm, with the potential for modest upward pressure in the second half of 2026. This reflects the interaction between above-target inflation persistence and weaker underlying growth, compounded by energy-related price pressures.

By contrast, China is expected to maintain a slightly easing bias in rates through H2 2026, as policy support is directed toward stabilising domestic growth amid relatively subdued inflation dynamics.

Japan remains the key outlier, with a gradual continuation of policy normalisation. Rates are expected to increase incrementally as inflation stabilises closer to target and wage growth strengthens, supporting a steady exit from ultra-loose monetary policy conditions.

Interest Rate Expectation (%)

Interest rate trends for major economies (US, EA, UK, China, and Japan) from 2021 to 2026

Structurally, the current interest rate environment reflects a clear shift in global monetary policy regimes. After a prolonged period of historically low rates through 2021, central banks initiated one of the most aggressive tightening cycles in decades during 2022–2023, led by the US and UK, with the Eurozone following thereafter. China’s policy stance remained comparatively stable over this period, while Japan maintained near-zero rates with only gradual adjustments.

From 2024 into 2025, policy rates began to ease modestly across developed markets. However, they have remained structurally higher than pre-2022 levels, signalling a sustained period of tighter financial conditions relative to the previous decade.

In 2026, most major central banks are expected to pause or slow their easing cycles following significant rate cuts in 2025. This reflects a reassessment of inflation risks, particularly in light of rising energy prices and renewed geopolitical tensions, which have reintroduced upside pressure on inflation expectations.

Japan remains the key exception, continuing on a gradual tightening path as it transitions away from decades of ultra-accommodative monetary policy, supported by stronger wage growth and more persistent domestic inflation dynamics.

Structural Investment Themes & Key Risk Monitor

The macro environment reinforces two structural investment themes that remain increasingly relevant for long-term portfolio positioning, alongside one key sovereign risk area to monitor.

1. Critical and Rare Earth Minerals

Critical minerals, particularly rare earth elements, are critical inputs across defence, AI infrastructure, electrification, and the broader energy transition, including applications in missiles, drones, EVs, renewables, and data centres.

Demand is being structurally driven by rising global defence spending (towards 2–3% of GDP in several economies), rapid AI infrastructure expansion (hyperscalers approaching USD 400bn annual capex), and continued EV adoption, with further intensity from energy-hungry AI data centres.

Supply remains highly constrained and geographically concentrated, with China accounting for the majority of rare earth production and dominating refining and magnet manufacturing, while Western economies remain import-dependent and exposed to processing bottlenecks.

Long project lead times further limit supply responsiveness, while geopolitical fragmentation is accelerating policy support for domestic supply chains, including US, Australia and Japan cooperation and EU critical minerals strategies.

Combined with increasing use of long-term offtake agreements and price support mechanisms, these dynamics reinforce a structurally tight market and support a positive long-term investment outlook across the critical minerals value chain.

2. Food Security

Food security is becoming an increasingly important structural driver within global markets, driven by increasing fragility across global agricultural systems, where concentrated supply chains, climate volatility, and geopolitical fragmentation are elevating long-term supply uncertainty and price risk.

Global food and input markets remain highly concentrated, with the top 3–5 exporters accounting for around 60–85% of trade in key staples and fertilizers, while reliance on a limited number of maritime chokepoints amplifies systemic vulnerability.

This is compounded by rising climate volatility disrupting yields in key producing regions and increasing frequency of extreme weather events. At the same time, recurring export restrictions and trade interventions (e.g., wheat export bans, Russia–Ukraine-related disruptions, and US–China soybean tariffs) reflect a structural shift from efficiency-driven globalisation to security-led fragmentation.

Fertilizers remain a key transmission channel, with nitrogen-based inputs closely linked to natural gas prices, embedding energy volatility directly into food inflation, while structurally tight and geopolitically exposed supply chains have led to persistent input price stickiness.

Overall, these dynamics support sustained pricing power and margin resilience across select parts of the agricultural value chain, particularly fertilizers, seeds, agrochemicals, and vertically integrated agribusinesses with global scale and trading capabilities.

3. Key Risk Monitor: Indonesia Sovereign Risk Downgrade Pressure

Indonesia is experiencing rising sovereign risk sensitivity, driven primarily by weakening perceptions of policy credibility rather than immediate macro stress.

Key concerns relate to fiscal discipline, institutional consistency, and policy execution, contributing to a higher risk premium across sovereign bonds, FX, and equities.

Pressures stem from expansionary fiscal policy, higher subsidy costs linked to energy volatility, and external shocks from geopolitical fragmentation, although fiscal policy remains anchored to a 3% of GDP deficit ceiling.

External balances are mixed, with energy import pressures offset by a strong commodity export base (palm oil, nickel, vehicles), providing a structural trade buffer.

Sovereign yields have risen, with 10-year bonds around 6.45%, reflecting higher risk premia and funding volatility.

The rupiah remains weak in the 16,800–17,500 per USD range, driven by capital outflows and energy exposure, partially offset by commodity FX inflows.

Equities are down 12% YTD 2026, reflecting macro repricing and sentiment-driven outflows rather than fundamental earnings deterioration.

Policy response has focused on subsidies, spending control, and fiscal rule adherence, but has not fully restored confidence. The key constraint is increasingly perceived to be policy predictability rather than macro capacity.

Overall, Indonesia remains fundamentally stable but is entering a higher volatility, elevated risk premium regime, with re-rating dependent on improvements in policy credibility and institutional consistency.

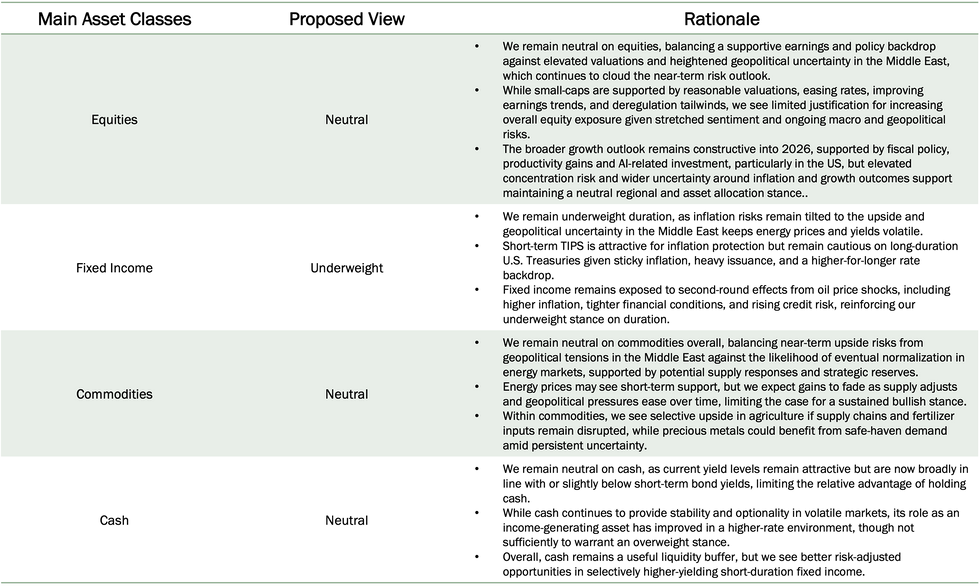

Asset Class Views

Equities

Comments