May 2026 Market Review: AI-Led Equity Rally Continues Amid Easing Geopolitical Tensions

- Tanooj Gopeechand

- Jun 5

- 5 min read

Updated: Jun 10

After April’s strong rally, markets remained constructive in May as investors continued to price in geopolitical de-escalation. Late in the month, a credible path toward an agreement between the US and Iran emerged. While negotiations were still ongoing at month-end, the probability of a resolution appeared increasingly high.

The prospect of easing energy tensions supported fixed income markets, reversing earlier yield increases. Against this backdrop, central banks are likely to remain cautious, given the risk of persistently elevated energy prices. Even in the event of a swift resolution, oil prices may remain above pre-crisis levels for some time, as supply recovery and logistical normalisation are expected to take several months.

Market and Macro Overview

May returns reflected a more selective risk-on environment than April. Positive fundamentals supported equity markets, which continued to register low volatility, despite the uncertain geopolitical context. Fixed income posted modest gains as longer-duration Treasuries and corporate bonds benefited from lower yields and stable credit conditions. In contrast, commodity markets moved sharply lower.

After a quiet month in May, major central banks look set to become increasingly focused on fighting inflation, as they attempt to counter mounting energy-driven stagflationary pressures, fuelling expectations of rates hikes as early as June.

CPI data signalled a renewed build-up in global inflationary pressures:

In the United States, April CPI rose 3.8% year-on-year, exceeding expectations and marking the fastest annual pace since early 2023. Core CPI increased by 2.8% year-on-year, supported by a rebound in housing-related components.

In Europe, inflation accelerated to 3.0% year-on-year, primarily driven by higher energy prices, particularly motor fuels. However, core inflation moderated to 2.2% year-on-year, reflecting softer services inflation. This was partly influenced by seasonal effects, as the earlier timing of Easter in 2026 shifted some travel-related price pressures from April into March.

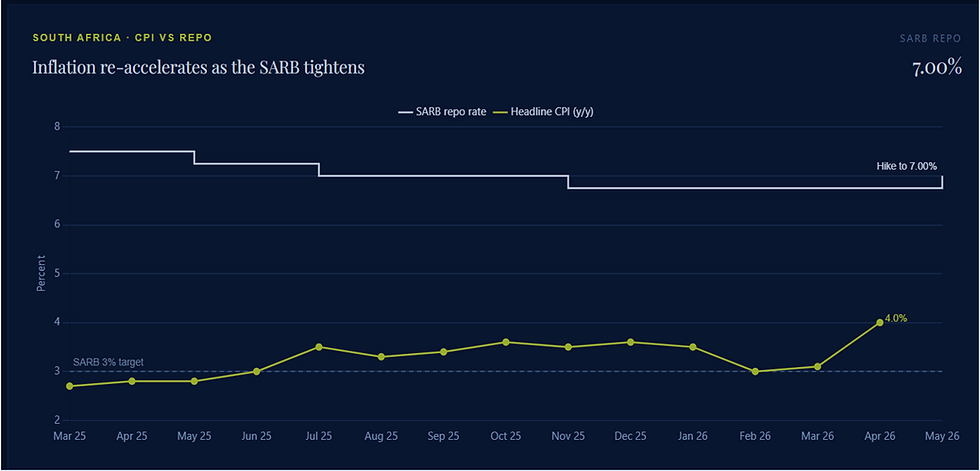

In South Africa, inflation accelerated from 3.1% in March to 4.0% in April, driven primarily by higher fuel prices linked to the Middle East conflict. Inflation is expected to average 4.4% in 2026 as second round effects gradually feed through the wider economy. The South African Reserve Bank (“SARB”) increased the repo rate by 25 bps to 7.0% due to upside risks to inflation, including the oil shock, higher fuel prices and greater uncertainty.

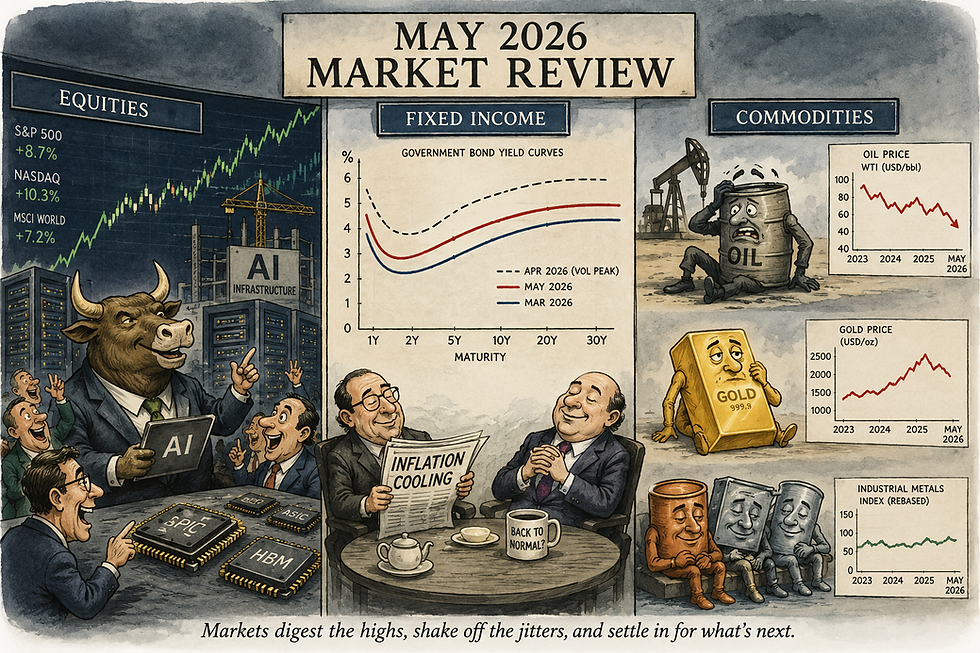

Equities overview

During the month, markets reached new highs after significant upward revisions in earnings expectations. Semiconductors, essential in the AI buildout, are leading earnings growth. The market is looking through the ongoing geopolitical tensions, but risks remain path dependent, particularly if energy disruption intensifies. Technology remains the leading sector for earnings growth, driven by AI. Since the popular launch of generative AI in late 2022, capex-led growth continues to dominate and is broadening as a driver for earnings growth expectations.

In the United States, the S&P 500 and the NASDAQ posted gains of 5.2% and 8.4% respectively. Both the S&P 500 and the NASDAQ recorded their strongest month since 2020. Market breadth weakened as the Technology sector was only sector to outperform the S&P 500 index. The rally was underpinned by renewed AI optimism and strong technical flows. Upbeat earnings releases provided further support for equities.

Europe's benchmark STOXX 600 index rose 2.4% in May. Most European markets finished higher as investors responded to improving risk sentiment and stronger technology shares. Developed market leadership shifted toward technology and export-oriented economies rather than commodity-driven markets.

Japan’s Nikkei 225 posted gains of 11.9% over the month. Japan’s first-quarter GDP growth beat expectations (+2.1% quarter-over-quarter), led mainly by consumption. Exports and public investment were also strong (+5.7%), supported by expansionary policies under the new prime minister. The positive economic data and AI-led enthusiasm supported Japanese equities.

Emerging market equities extended their advance in May, led once again by Asia’s technology exporters. The MSCI Emerging Markets Index gained 9.5%, outperforming most developed market benchmarks. Korea’s KOSPI surged 28.5% as investors continued to favour semiconductor and AI supply-chain exposure. In contrast, several commodity and domestic-demand markets struggled. Technology-driven export economies continue to attract capital while commodity-sensitive markets face increasing pressure. Indonesian stocks fell 11.1% month-on-month, while Indian and Chinese stocks remain negative for the year.

In South Africa, the FTSE/JSE All Share Index fell by 0.5% month on month, underperforming local bonds, following the SARB’s interest rate hikes to combat inflation, rendering bonds more attractive.

Fixed income overview

Early in May, bond markets weakened as stronger-than-expected US inflation data and a sharp rise in oil prices fuelled concerns over renewed inflationary pressure. These developments pushed global yields higher and led to a broad-based selloff across duration-sensitive assets.

As the month progressed, sentiment gradually shifted. Expectations of a de-escalation in Middle East tensions, particularly surrounding US–Iran negotiations helped ease fears of a sustained energy shock. Investors cautiously extended duration as inflation fears eased and bond market volatility declined. Government bonds delivered modest gains as yields stabilized after a volatile spring.

The U.S. Aggregate Bond Index gained 0.3%, while long-duration Treasuries outperformed. The S&P 20+ Year Treasury Index returned 0.5%, and the S&P 10-20 Year Treasury Index gained 0.45%.

South Africa’s FTSE/JSE All Bond Index returned 2.9% over the month. Emerging market government bonds outperformed all major bond sectors during the month.

Commodities overview

May saw commodities reverse course from previous gains in April as energy markets corrected on the back of increased prospects of a potential peace agreement being reached between U.S and Iran. While energy-linked commodities such as WTI crude oil and RBOB gasoline fell, industrial metals such as copper and aluminium benefited from continued industrial demand. Overall, the Bloomberg Commodity index declined by 3.8% month on month, implying energy weakness overwhelmed strength in industrial metals.

Brent crude oil prices posted losses of 19.3% over the month. On a year-to-date basis, WTI crude is however still up 52.1%. Despite May’s correction, commodities remain one of the strongest asset classes in 2026, with WTI crude being one of the major contributors to this outperformance.

Gold fell by 1.8% over the month as sentiment weakened towards month-end as markets increasingly priced in a potential de-escalation in the Middle East, reducing demand for defensive assets. At the same time, expectations of a more hawkish Federal Reserve limited upside momentum for non-yielding assets such as gold.

Conclusion

The prospect of a US–Iran agreement, alongside expectations of a gradual reopening of the Strait of Hormuz, represents a clear improvement in the geopolitical backdrop. Market focus is likely to shift toward the pace and credibility of the peace process, with the speed of normalisation in maritime transit conditions playing a key role in determining how contained the broader economic impact of the energy shock ultimately proves to be.

A normalisation of conditions is broadly supportive for both equities and fixed income. However, equities have remained relatively resilient throughout the Middle East tensions, supported by strong corporate fundamentals, and may already be partially pricing in a favourable resolution. In contrast, bond markets stand to benefit more directly from easing inflation expectations and a reduction in energy-driven price pressures.

As conditions stabilise, attention may also return to earlier-year investment themes, including the case for broader geographic diversification away from the US, particularly toward Europe and emerging markets and the view that the US dollar may be losing some of its traditional safe-haven characteristics.

Comments