Three Years On: Is the Bull Market Running Out of Steam or Just Getting Started?

- Girish Appadu

- Oct 27, 2025

- 2 min read

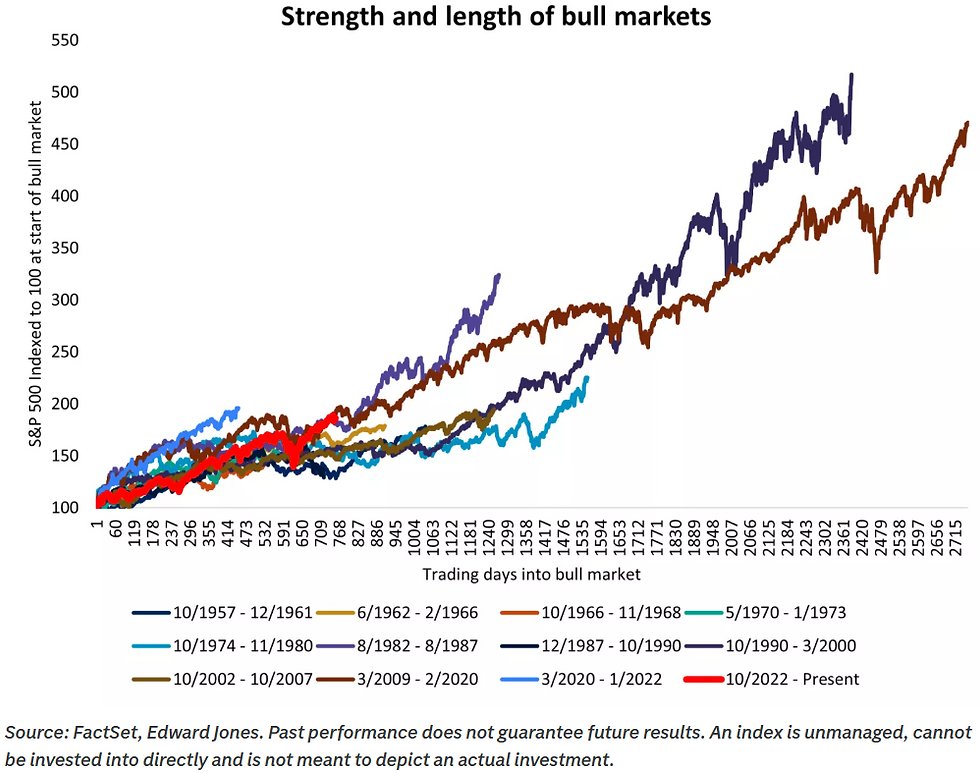

Equity markets have reached a remarkable milestone: the current bull market has officially turned three years old. Few would have predicted such resilience back in October 2022, when markets bottomed amid surging inflation, aggressive rate hikes and widespread investor pessimism. Since then, global indices have nearly doubled, driven not just by macro recovery but also by breakthroughs in technology and AI, reshaping corporate growth and investor confidence.

The “wall of worry” remains real:

Geopolitical tension and fragile trade relationships are creating uncertainty.

Slowing employment data has masked underlying risks.

Elevated AI valuations are prompting questions about how much optimism is already priced in.

Yet markets are climbing, supported by moderating policy conditions. U.S. inflation is easing and the Federal Reserve may begin easing rates in late October, potentially followed by another cut before year-end. Cheaper capital could extend the economic cycle, supporting earnings growth and risk appetite.

Corporate earnings remain a key driver. Early Q3 results highlight stable margins, disciplined cost management and strong demand in AI infrastructure and cloud services. Companies that convert investment into productivity are likely to be rewarded, particularly in AI and automation.

Looking ahead, the bull market appears to be transitioning from policy-driven expansion to earnings-led progression, which may bring more selective volatility. Investors can expect:

Short-term consolidation as markets digest recent gains.

Sector rotation, with industrials, health care and consumer discretionary catching up to technology leaders.

Regional broadening, as international and emerging-market equities regain momentum amid a softer U.S. dollar and stabilising global trade conditions.

We view the market as firmly mid-cycle, with compelling opportunities for disciplined investors. Balancing growth-oriented equities with quality and valuation focus, diversifying across sectors and regions and maintaining fixed-income exposure for stability can position portfolios to capture the next wave of gains. While short-term volatility is inevitable, solid fundamentals, ample liquidity and supportive policy measures point to continued upside potential in the long run.

Bottom line: This is not the beginning of the end; it is the next phase of a durable expansion. Investors should focus on long-term growth opportunities, sector rotation, and geographic diversification to navigate the evolving market landscape successfully.

Comments