2025: From Tariff Turbulence to Global Triumph

- Girish Appadu

- Jan 7

- 2 min read

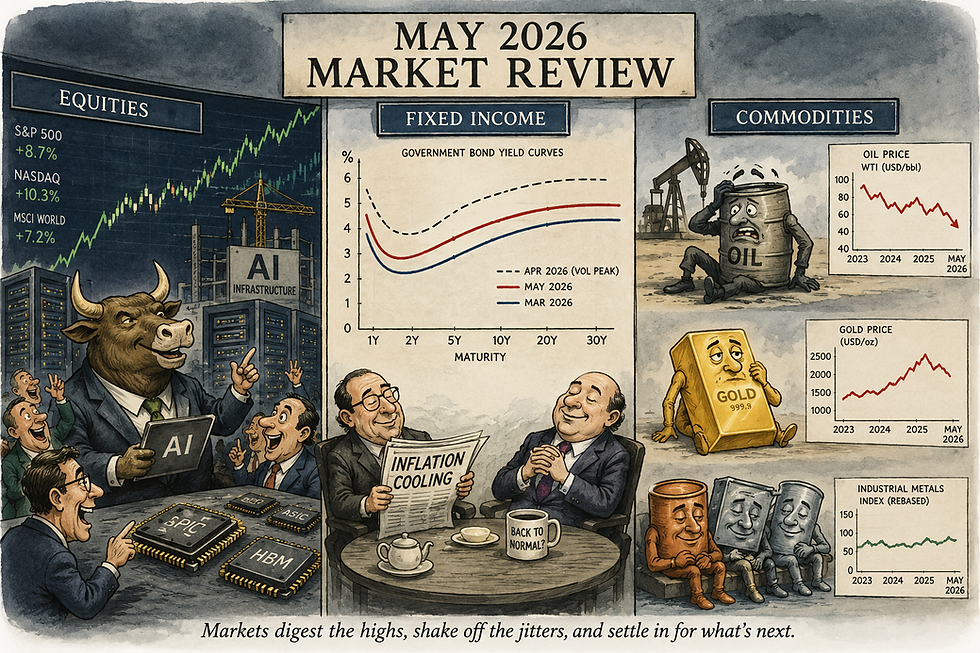

2025 defied early-year pessimism. The first half was dominated by trade concerns as US tariffs rose to levels not seen since the 1930s, triggering a sharp drawdown in developed market equities in April. Yet by year-end, a powerful “risk-on” turn, fueled by fiscal support, monetary easing and improving sentiment, drove an “everything rally.” It was the first year since the pandemic in which all major asset classes posted positive returns.

Performance broadened beyond the US, led by emerging markets and precious metals, while global bonds benefited from easing inflation fears and a weaker US dollar. Currency moves amplified returns for European and Emerging market investors. The dominant US equity theme remained Artificial Intelligence (AI) but 2025 marked a notable regime shift: for the first time in two decades, the S&P 500 was the weakest major equity market relative to peers.

Equities

Developed markets rebounded from a mid-year drawdown to finish over 20%.

Emerging markets outperformed, supported by broad-based strength and currency tailwinds.

Sector & region dynamics:

In the US, Communication Services and Information Technology led (+33.0% and +23.6%), though only two of the “Magnificent Seven” beat the S&P 500 as investors became more discerning about AI’s eventual winners.

South Korea topped global performance, helped by AI enthusiasm, governance reforms and attractive starting valuations.

Fixed Income

Global bonds returned +8.2% (USD), with declining inflation risks and rate cuts supporting total returns.

Emerging market debt was the top fixed income performer, bolstered by solid fundamentals and currency appreciation.

Global credit delivered as spreads compressed across investment grade and high yield; defaults edged up but corporate balance sheets remained broadly resilient.

Central Banks

Federal Reserve (US): Cut rates by 75 bps in H2 2025 as inflation pressures eased and labour market indicators softened.

Bank of England (UK): Reduced rates by 100 bps amid cooling wage pressures and a weakening labour market, helping Gilts’ positive annual returns.

Bank of Japan (Japan): Continued normalisation with yields rising as markets priced in further fiscal stimulus and longer-term debt sustainability concerns.

Views

Diversification remains paramount. 2025 demonstrated the power of balanced allocations across regions, sectors and asset classes, particularly when currency moves are material.

Currency exposure is a performance lever. Dollar weakness amplified non-US returns in 2025; investors should consider currency in both risk management and opportunity capture.

AI leadership will evolve. Market breadth within AI is increasing as profitability, capital intensity and supply-chain realities come into focus. Stock selection matters more than ever.

Fixed income is investable again. Attractive starting yields, moderating inflation and selective spread opportunities support a constructive view on quality credit and parts of EM debt.

Regional nuance matters. Korea’s reset, Latin America’s currency impulse, Europe’s currency tailwind and Japan’s policy normalisation each create distinct return drivers and risks.

Positioning for 2026

Maintain core global diversification with calibrated exposure to EM equities and quality global credit.

Use active currency management to enhance return potential and mitigate downside.

Comments